Strategy Design Write-Up: Triple EMA v.1

This strategy (yet again) uses one of my favourite indicators, the exponential moving average (EMA). Here's what I did differently.

Hey guys!

This is going to be another post on strategies that I have backtested and my thoughts on the strategy performance, as well as the backtest procedure and guidelines. I appreciate any and all feedback or suggestions you may have that may improve either the post layout, or the strategy design itself. Hope you continue to enjoy this series.

Part 1: The Strategy Ruleset

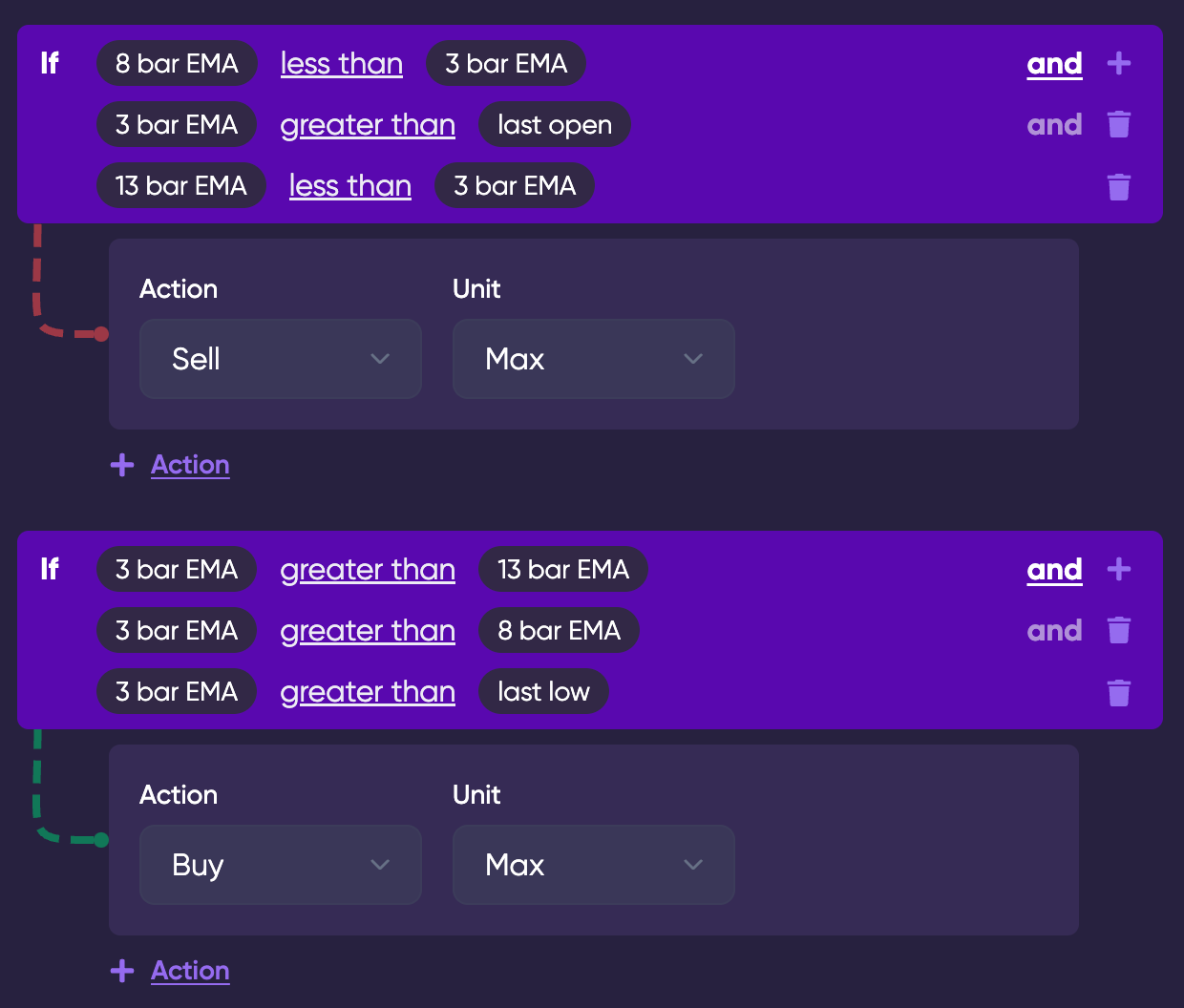

This strategy yet again uses one of my favorite indicators, the exponential moving average (EMA). This time, I use 3 different EMA lengths to form a triple EMA strategy. The entry criteria is based on a 3 bar EMA being greater than all of a 13 bar, an 8 bar, and the last low price. This should represent a very fast increase in price, and strong momentum.

The exit criteria is based on the 8 bar and the 13 bar being less than the 3 bar EMA, and the opening price being below the 3 bar, meaning it has crossed it to the downside. This should represent a change in momentum.

Part 2: The Assets Traded

After thinking over the problems with the assets in my last post, I came to the conclusion that I needed more stocks, and more randomness in my selection. Therefore I ran a screener (a new function of Pluto), and randomly chose some stocks from that, along with the usual FAANG. I hoped that this would provide a more accurate, and realistic backtest result.

The screener would not load for me during the backtest (a possible issue on my end), so I manually inputted my random selection of stocks. The screener settings can be seen below:

Part 3: The Settings

The settings are the same as usual. Nothing too important!

Part 4: The Backtest Scenario

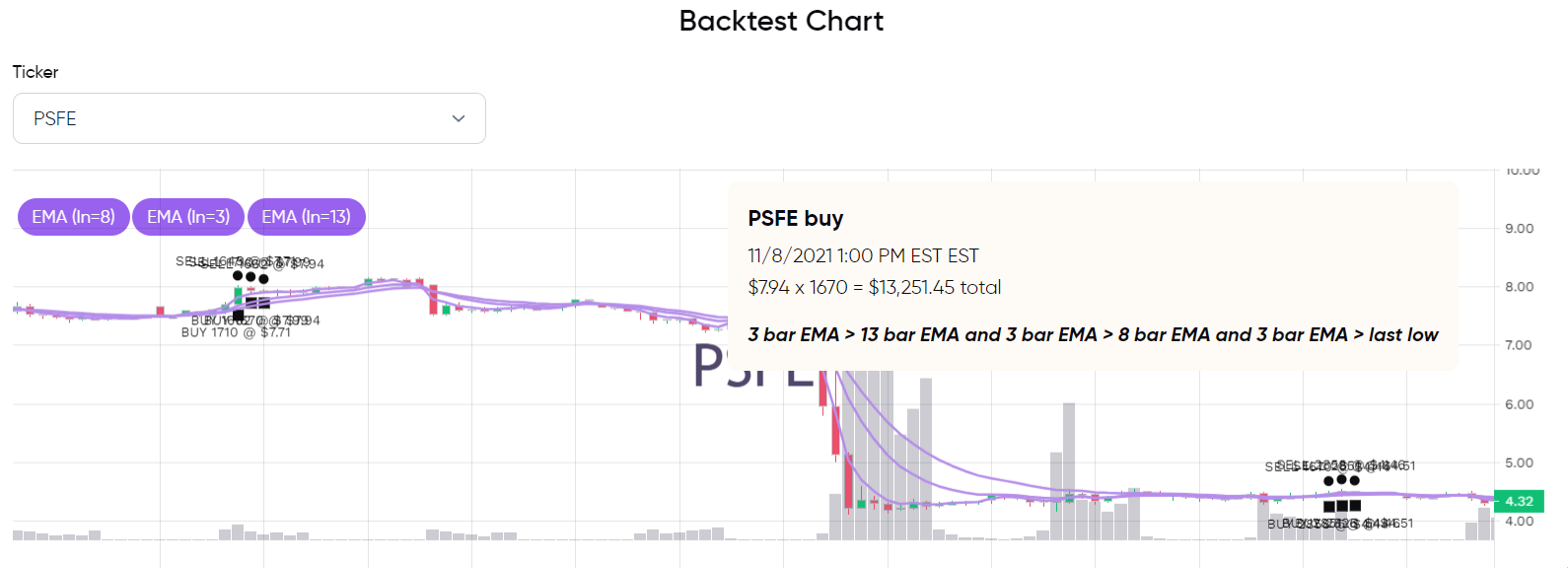

Part 5: The Results

C....not quite satisfactory. Seems to have some good points, but not profitable. I am going to take a closer look into the results.

So, it returned more than buying and holding would have (for all that is worth lol), and had a high win rate. I might be able to find something to help optimize the strategy in the win rate:

Looks like there were a good few large losses within the trades taken, which heavily offset all of the small wins. Only 1 win over 25%, yet 10 losses of over 25% - rough. Maybe better exit criteria could help with this.

Worst trade:

I tested with a few variations on the 3 bar being greater than open, close, low and high, none of which produced better results.

Part 6: Potential For Optimization

- Different exit criteria

- Different timeframe

- Greater length of backtesting period

Hope you all enjoyed this post!